India’s financial landscape is undergoing a transformative shift, fuelled by a confluence of factors. A decade-long surge in wealth has seen AIF funds experience more than 100-fold increase in AUM, boasting a robust 56% CAGR between FY14 (Rs 0.13 lakh crore) and FY24 (Rs 11.35 lakh crore). The growing population of affluent Indians (ultra HNIs), projected to double by 2026 as per a Knight Frank Wealth Report, have created a fertile ground for diverse investment opportunities in AIFs.

India’s booming economy and youthful demographic profile have positioned it as a prime market for alternative investments. SEBI, recognising this potential, has taken proactive steps to modernise the regulatory framework for AIF funds. Recent circulars issued in 2024 aim to streamline processes, enhance transparency, and address emerging challenges in these investment products. These initiatives show the regulator’s commitment to fostering a robust and investor-friendly financial ecosystem.

As India continues its trajectory of growth, it is poised to become a global financial hub. The increasing sophistication of Indian investors, coupled with a conducive regulatory environment, will further propel the growth of alternative investments.

Here is a look at a few of these circulars on AIF funds and their implications for investors.

In a circular dated April 26, 2024, SEBI introduced a framework allowing Category I and II AIFs to create encumbrances on their equity holdings in investee companies. That is, AIF funds can pledge their shares in investee companies. This move aims to ease debt raising for these companies, particularly those operating in infrastructure sectors. While this provides much-needed flexibility, it is crucial to understand the accompanying conditions:

The circular mandates the Standard Setting Forum for AIFs (SFA) to develop implementation standards ensuring proper encumbrance utilisation. Compliance with these provisions forms a crucial part of the AIF’s Compliance Test Report.

Thus, share pledging by AIFs in infrastructure companies is like a double-edged sword. This strategy is not without its risks. Fluctuations in share prices can expose AIFs to potential losses and the risk of default by the investee company can damage the fund’s reputation.

However, it enables AIFs to unlock additional capital, enhance returns, and adapt to market dynamics. By using their existing equity investments as collateral, AIFs can secure loans without liquidating their assets, thereby maximizing returns for both the fund and its investors.

In another circular issued on April 29, 2024, SEBI eased the process for AIFs to intimate changes in their PPMs (private placement memorandum) by exempting certain changes from the mandatory involvement of a merchant banker. This relaxation aims to reduce compliance costs and streamline procedures for AIFs. That is, PPMs of AIF funds can be submitted directly to the regulator rather than through a merchant banker.

PPM is a key document for AIF funds which discloses essential information to investors, following a mandated template. These include fee details, history, exit process and more.

A detailed list of changes eligible for direct filing with SEBI is also mentioned in the circular. These include updates to market outlook sections, changes in contact details or service providers, adjustments to fund size or commitment periods, and the inclusion of new disclosures mandated by regulations.

Large Value Funds for Accredited Investors receive further exemption, allowing them to directly file any PPM changes with SEBI, accompanied by an undertaking signed by key personnel of the AIF Manager.

Based on the circular issued on October 8, 2024, SEBI underlined the commitment to investor protection and regulatory compliance by strengthening due diligence requirements for AIFs, their managers, and key personnel.

SEBI identified specific areas requiring stringent due diligence checks:

The market regulator further mandates adherence to implementation standards developed by SFA for conducting these due diligence checks. The circular outlines consequences for failing these checks, including the exclusion of problematic investors or the complete prohibition of the investment. Existing investments also fall under the purview of these due diligence requirements, with reporting obligations for non-compliant investments.

Another circular provides AIFs and their investors with much-needed flexibility in managing unliquidated investments during the closing stages of a scheme. It introduces the concept of a ‘Dissolution Period’, providing an additional avenue for liquidating remaining investments after the initial Liquidation Period.

The Dissolution Period requires approval from at least 75% of investors and necessitates specific conditions, including arranging bids for a minimum percentage of unliquidated investments.

The circular also introduces mandatory in-specie distribution of unliquidated investments if the AIF funds cannot secure the required investor consent for the Dissolution Period or in-specie distribution during the Liquidation Period. This provision streamlines the process for handling unliquidated assets, ensuring a clear path forward even when consensus is challenging.

Recognising the challenges faced by schemes with expiring Liquidation Periods, the circular grants a one-time extension to schemes whose Liquidation Period expires on or before July 24, 2024. This fresh Liquidation Period extends to April 24, 2025, providing these schemes with additional time to liquidate their assets or utilize the newly available options for handling unliquidated investments.

Finally, SEBI discontinued the option of launching new Liquidation Schemes from April 25, 2024, onward, while existing Liquidation Schemes will continue to operate under the previous regulations.

Takeaway

Changes like simplification in PPM and addressing emerging challenges like liquidation period extensions foster an environment of ease while also ensuring transparency for AIF Funds in India, a segment that has seen a massive spike in assets under management. The recent regulatory measures reflect SEBI’s commitment to promoting a healthy AIF ecosystem as India continues its trajectory of growth and aims to become a global financial hub.

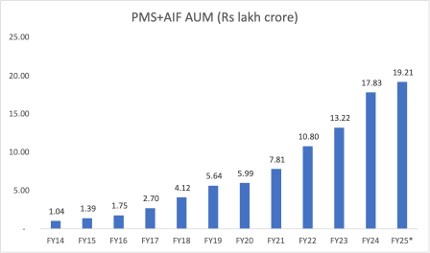

A significant growth of alternative investments in India is seen in both Portfolio Management Services (PMS) and Alternative Investment Funds (AIFs), driven by the country’s economic expansion and the evolving investment preferences of High-Net-Worth Individuals (HNIs) and Ultra-High-Net-Worth Individuals (UHNIs).

Source: SEBI

Before we dive into the growth of Indian alternative investments, let’s understand the changes in preferences a bit more.

Rising Demand for Wealth-Building Products

India’s robust economic growth, coupled with increasing disposable income among HNIs and UHNIs, has fueled a surge in demand for sophisticated investment avenues, leading to significant expansion in the alternative investment landscape.

Source: The Knight Frank Wealth Report, 2022, 2023, *estimated.

This trend is driven by investors seeking to diversify their portfolios beyond traditional assets and achieve higher returns. Notably, the Indian alternative investment industry (PMS invest & AIF fund) has exhibited a remarkable compound annual growth rate (CAGR) of 33% over the past decade (FY14 to FY24). As India aims to become a $10 trillion economy by 2035, alternative investments are expected to play a crucial role in wealth creation.

Shifting Investment Preferences

While the Indian equity market has performed well in recent years, HNIs and UHNIs are increasingly seeking alternative investment options to optimise their wealth. A report by 360 ONE Wealth and CRISIL highlights a shift away from traditional investments, with UHNIs and HNIs showing growing interest in alternatives such as PMS funds, AIF funds, Real Estate Investment Trusts (REITs), and private equity, aiming for annual returns of 12-15%. The report also notes that 41% of HNIs and UHNIs work with multiple wealth management firms, indicating a preference for professional advice in managing their investments. This trend is particularly prevalent among those under 40.

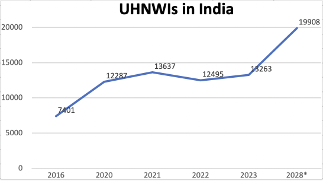

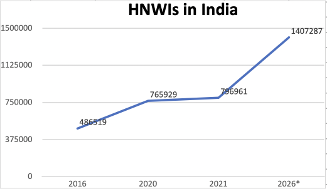

The rapid growth of alternative investments, surpassing the growth rates of mutual funds and other asset classes over the past five years, underscores their appeal. The Knight Frank Wealth Report projects a 50% increase in the number of UHNIs by 2028, while HNIs are expected to more than double by 2026 in India. This expanding pool of capital is actively seeking alternative investment options with the potential to deliver higher returns than traditional instruments.

Growth of PMS and AIFs

The rising income levels and specific investment objectives of HNIs and UHNIs are driving the demand for specialized PMS funds and AIF funds tailored to meet their unique needs. The PMS industry in India has witnessed consistent growth, with Assets Under Management (AUM) managed by PMS providers increasing at a CAGR of 23% over the past decade (FY14 to FY24). The AUM reached Rs 7.43 lakh crore as of September 2024.

While PMS services has seen a strong growth, it is the AIF fund industry that has really taken off.

AIFs, privately pooled investment vehicles offering flexibility in investment strategies and asset classes, have exhibited even more impressive growth, achieving a CAGR of 48% over the past ten years (FY15 to FY25 – Q1FY25). Their AUM now stands at Rs 11.78 lakh crore as of June 2024. This growth is primarily attributed to the increasing popularity of Category II AIFs, which encompass private equity, private credit, real estate funds, venture capital, venture debt, and infrastructure funds. Notably, real estate has emerged as the top sector, contributing 17% of investment by AIFs.

Within Category II AIFs, the majority of investments have been directed towards private equity, followed by private credit, infrastructure funds, and real estate according to many experts. This category has experienced tremendous growth with a CAGR of 65% in the past decade!

Drivers of Growth in AIFs

Several factors contribute to the remarkable growth of AIFs in India:

First, India’s position as a top-five global economy, along with its youthful demographic profile, provides a strong foundation for AIF funds. This along with increasing income levels, growing investor awareness, and supportive regulatory reforms are fuelling the AIF industry’s growth.

Also, expanding infrastructure, a thriving start-up ecosystem, and a conducive business environment contribute to the success of AIFs. Another reason is India’s burgeoning start-up ecosystem, with a projected 250 unicorns by 2025, presents significant opportunities for AIFs to provide tailored solutions like venture debt.

But most importantly, alternative investments, both PMS and AIF, offer investors a diverse range of opportunities to diversify their portfolios across listed and unlisted equities, fixed-income instruments, and other asset classes and provide an opportunity for superior returns.

Outlook

The Indian alternative investment industry, with its current AUM of Rs 19.21 lakh crore (approximately $0.23 trillion), has significant room for growth compared to the global AUM of $16.78 trillion. Preqin forecasts the global alternatives industry to reach $29.2 trillion in AUM by 2029.

If this growth trajectory continues, the overall industry is projected to surpass Rs 100 lakh crore by 2030, marking an over 5-fold increase in just 6 years, as per PMS Bazaar estimates. However, the potential for long-term growth depends on sustained economic growth, favourable economic conditions, and continued investor interest.

References:

https://s3.ap-south-1.amazonaws.com/x-docket.360.one/360_ONE_The_Wealth_Index_52805944da.pdf

https://www.fortuneindia.com/long-reads/aif-demand-signals-focus-on-wealth-creation/118282

https://www.sebi.gov.in/statistics/1392982252002.html